Important Questions

Multiple Choice Questions-

Q.1 Goods lost by fire should be credited to:

a) Trading A/c

b) Loss by Fire A/c

c) Sales A/c

d) Profit & Loss A/c

Q.2 Sales of Rs.10,000 recorded as Rs. 1,000 is an example of:

a) Compensating Error

b) Errors of principle

c) Errors of omission

d) Errors of commission

Q.3 Trial Balance might match in spite of presence of:

a) Errors of complete omission, Errors of principle

b) Errors of complete omission

c) Errors of commission

d) Errors of principle

Q.4 Compensating errors are of a ___________ nature.

a) Neutralizing

b) Consistent

c) Concealing

d) Accommodating

Q.5 Rectification entries are passed in -

a) Journal Proper

b) Purchase Book

c) Sales Book

d) None of the options

Q.6 Under casting of Sales book is corrected by______Sales Account

a) Crediting

b) Debiting

c) Balancing

d) Ignoring

Q.7 A Suspense Account will give the

a) Debit or Credit balance

b) Debit balance

c) Credit balance

d) None of the options

Q.8 Purchase of office furniture worth Rs. 5,000 has been debited to General

expenses account. Identify the error.

a) Error of Principle

b) Clerical error

c) Error of omission

d) None of the options

Q.9 Rs. 2000 received from Smith whose account was previously written off as bad

debt should be credited to -

a) Bad debts recovered Account

b) Smiths Account

c) Cash Account

d) None of the options

Q.10 A Trial Balance is prepared to

a) Ensure Arithmetical accuracy

b) Locate Errors of Principle

c) Locate Errors of omission

d) Locate Errors of commission

Very Short-

1. Define trial balance?

2. Explain two objectives of preparing a trial balance.

3. While preparing a Trial balance which error cannot be disclosed.

4. State one example of an error of commission?

5. Define a compensating error.

6. Give an example of principal error.

Short Questions-

1. If the amount is posted in the wrong account or it is written on the wrong side of

account, what error is it?

2. What do you understand by rectification of errors?

3. Give two examples of two-sided error.

4. Give one example of one-sided errors.

5. Discuss the balance method of preparing trial balance.

Long Questions-

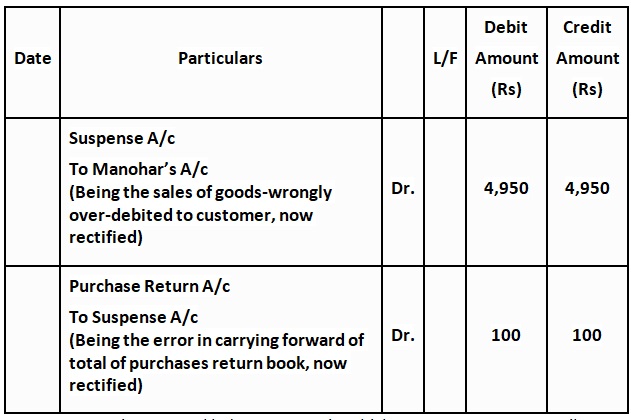

1. A book-keeper of a trading concern having failed to agree the trial balance, opened a suspense account

and entered the difference in the trial balance.

i. Goods sold to Manohar for Rs 550 was posted as Rs 5,500.

ii. Purchases return book was carried forward as Rs 1,220 instead of Rs 1,120.

You are required to pass the journal entries for rectification of the above errors

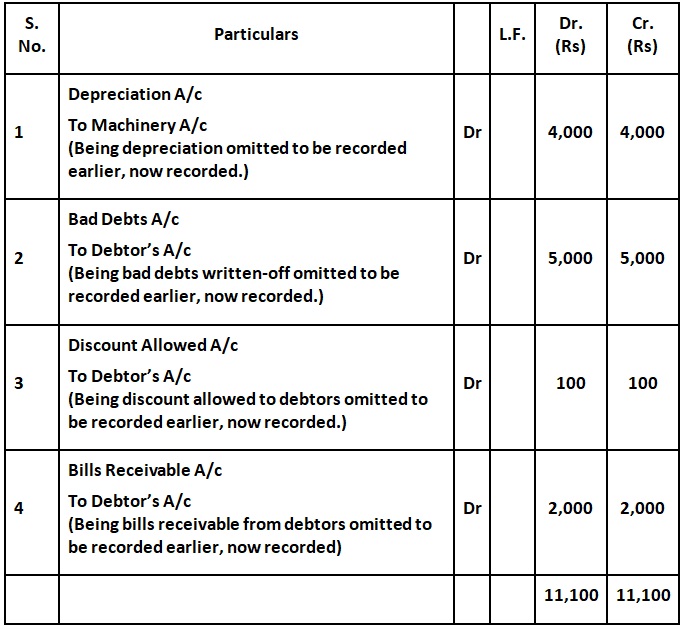

2. Rectify the following errors

i. Depreciation provided on machinery Rs 4,000 was not posted.

ii. Bad debts written-off Rs 5,000 were not posted.

iii. Discount allowed to a debtor Rs 100 on receiving cash from him was not posted.

iv. Bill receivable for Rs 2,000 received from a debtor was not posted.

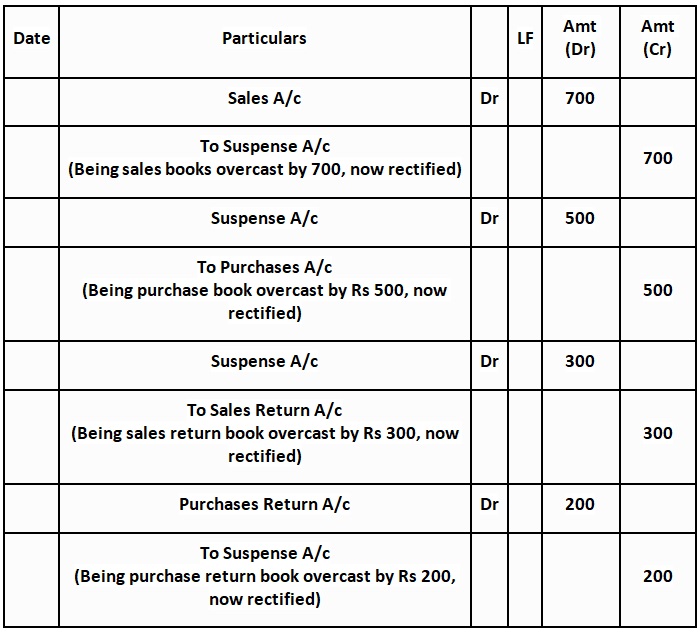

3. Rectify the following errors

i. Sales book overcast by Rs 700.

ii. Purchase book overcast by Rs 500.

iii. Sales return book overcast by Rs 300.

iv. Purchase return book overcast by Rs 200

Case Study Based Question-

1. Read the following hypothetical text and answer the given questions: -

An accountant while balancing his books on 31st December 2016 found that there was a difference of

₹270 in the trial balance. Being required to prepare the final accounts he placed the difference to a newly

opened Suspense A/c, which was carried forward to the next year when the following errors were discovered:

Salary for the month of March was posted twice ₹155.

Interest on investment collected by the bankers, were posted directly in concerned accounts through the pass

book, but no entry was made in the bank column of the cash book ₹75.

Rent of ₹350 received from Ashok credited both to Rent Account and Ashok Account.

A purchase of a chair from Karnal Furniture Mart for ₹65 has been entered in the purchase book as ₹56.

Old Machinery sold to the proprietor Keshav for ₹400 was entered in the Sales Book as sale to Kishore.

Cash Purchases from Ajay ₹189 were recorded in Cash Book as well as in Purchases Book and posted from both.

Closing Stock has been undervalued by ₹300.

The Profit & Loss Account disclosed a net profit of ₹15,000 for the year ended 31st March 2016.

Questions:

1. What will be the journal entry for the balance of Profit and Loss Adjustment Account?

(a) Profit & Loss Adjustment A/c Dr. 300

To Suspense A/c 300

(Being balance of Profit & Loss Adjustment A/c transferred to Suspense A/c)

(b) Profit & Loss Adjustment A/c Dr. 300

To Capital A/c 300

(Being balance of Profit & Loss Adjustment A/c transferred to Capital A/c)

(c) Profit & Loss Adjustment A/c Dr. 300

To Profit & Loss Appropriation A/c 300

(Being balance of Profit & Loss Adjustment A/c transferred to Profit & Loss Appropriation A/c)

(d) No entry will be passed.

2. What will be the rectification entry of the salary for the month of march posted twice?

(a) Suspense A/c Dr. 155

To Profit & Loss Adjustment A/c 155

(Being rectification of salary posted twice in the books)

(b) Suspense A/c Dr. 310

To Profit & Loss Adjustment A/c 310

(Being rectification of salary posted twice in the books)

(c) Profit & Loss Adjustment A/c Dr. 155

To Suspense A/c 155

(Being rectification of salary posted twice in the books)

(d) Profit & Loss Adjustment A/c Dr. 155

To Suspense A/c 155

(Being rectification of salary posted twice in the books)

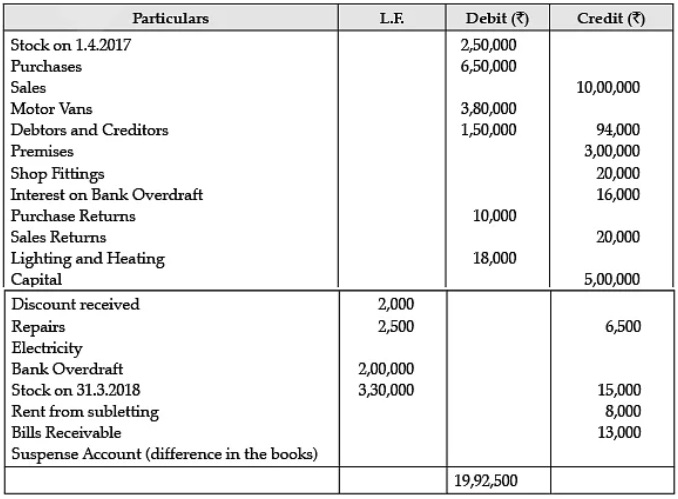

2. Read the following hypothetical Trial Balance extracted from the books of M/s Ravilal and Company

and answer the given questions:

In the books of M/s Ravilal and Company

Trial Balance as on 31/3/2018

Questions:

1. Which of the following items appears on the wrong side of the trial Balance?

(a) Purchases

(b) Motor Vans

(c) Premises

(d) Capital

2. What should be the actual total in the rectified Trial Balance?

(a) ₹18,21,000

(b) ₹19,92,500

(c) ₹19,21,000

(d) ₹18,92,500

Answer key

MCQ Answers-

1. Answer: Trading A/c

2. Answer: Compensating Error

3. Answer: Errors of complete omission, Errors of principle

4. Answer: Neutralizing

5. Answer: Journal Proper

6. Answer: Crediting

7. Answer: Debit or Credit balance

8. Answer: Error of Principle

9. Answer: Bad debts recovered Account

10. Credit; Ensure Arithmetical accuracy

Very Short Answers-

1. A trial balance is a worksheet record book that reflects the debit and credit balance of all the registered

accounts. This worksheet statement is used to prepare the final account report of the company. Trial balance

also determines the accuracy of the account. However, it doesn’t ensure that the account is error-free but surely

gives mathematical precision. AnsThe debit balance in passbook means overdraft.

2. Ans. The two objectives of preparing a trial balance

• To determine the financial accuracy of the ledger accounts

• To help in finding an error.

3. While preparing a Trial balance the following errors cannot be disclosed

• Error of Omission

• Error of Commission

4. Ans.Error of commission can be represented by the following example:

Purchase of goods for ₹5,000 entered in the purchase book as ₹500.

5. Ans. A compensating error can be defined as when one error compensates or neutralizes the other error.

6. Ans. Principal error can be represented by the following example:

When a purchase of furniture is debited to purchase account instead of a furniture account.

Short Answers-

1. Ans. Give one example of one-sided errors.

2. While recording business transactions, some errors are committed.There are 4 kinds of errors, namely;

• Error of Principle

• The error of Commission.

• Error of Omission

• Compensatory Error.

These errors have to be corrected before finalization of account. The process of correcting these errors

is known as Rectification of Errors.

3. Ans. Two-sided errors refer to those errors that do not affect the agreement (tallying) of the trial balance.

• Machinery purchased recorded in the purchases book.

• Old furniture sold is recorded as sales of goods.

4. Errors due to partial omission is an example of one-sided error.

5. Ans. Trial balance is a statement that is prepared to make sure that the transactions for a particular period

have been duly recorded in the journal and properly posted to the relevant ledger accounts. It has debit and credit

columns to record the balances extracted from ledger accounts with a view to test the arithmetical accuracy of the

books of accounts. Under balance method the following procedure is adopted to draw up a trial balance:

i. First of all the name of all accounts is written along with serial number.

ii. The total balances of all accounts are taken and debit balances are written in the debit column & credit balances in the credit column in the Trial Balance.

iii. The total of debit & credit columns of the Trial Balance is calculated. Total of both columns of Trial Balance should be equal.

Long Answers-

1.Answer - Journal

A suspense account is a general ledger account in which amounts are temporarily recorded. The suspense account

is used because the appropriate general ledger account could not be determined at the time that the transaction was recorded.

2. Rectification Journal Entries

3. Answer

In all the given cases, one-sided errors can be discovered as there has been an overcasting of the accounts.

Therefore, the rectification has been done by reversing the accounts opposite to their normal balance.

Case Study Answer-

1. Answer:

1. (b)

Solution: The journal entry for the balance of Profit and Loss Adjustment Account

Profit & Loss Adjustment A/c Dr. 300

To Capital A/c 300

(Being balance of Profit & Loss Adjustment A/c transferred to Capital A/c)

2. (a)

Solution: The rectification entry of the salary for the month of march posted twice

Suspense A/c Dr. 155

To Profit & Loss Adjustment A/c 155

(Being rectification of salary posted twice in the books)

2. Answer:

1. (c) Premises

Solution: Premises is an asset for business and like all other assets of business which has debit balance

as normal default balance it also has debit balance.

2. (a)₹18,21,000

Solution: The actual total in the rectified Trial Balance is ₹18,21,000.