Trial Balance And Rectification Of Errors

Meaning of Trial Balance

Trial balance is a statement prepared to check the arithmetical accuracy of transactions recorded in the journal and those

posted to the ledger and balanced the ledger accounts. The balance of ledger accounts shows the difference between the total

of the debit items and credit items in an account. A debit balance shows the total of debit items greater and a credit balance

shows the total of credit items greater. These debit and credit balances are posted in the respective column of the trial balance.

According to the double entry system, each debit item has a corresponding credit item. Hence, the total of the debit and credit

balances are equal for different accounts in the ledger. When the debit and credit balances are equal in the trial balance, it is clear

that all the posting and balancing of accounts are arithmetically correct.

According to Carter, a trial balance is the list of debit and credit balances, taken out from the ledger. It also includes cash and

bank balances taken from the cash book.

Features of Trial Balance

It is a complete record of all ledger accounts and cash book

It is prepared as a result of the double entry system of book keeping, thought it is not a part of it.

It assists in verifying the arithmetic accuracy of posting entries from journal to ledger accounts

It is not completely accurate to take any decision because there are some errors not disclosed in this trail

balance. It doesn’t disclose some of the errors because of which it is not considered as absolute proof of accuracy.

It is prepared on a particular date and considered as a working paper.

Functions of Trial Balance

It helps to ascertain the arithmetical accuracy of ledger accounts.

It assists in preparing the financial statement

It provides a summary of the ledger accounts

It identifies the errors in book keeping work but does not disclose all the errors in book keeping.

Debit Balances- Assets, debtors, drawings, expenses and losses

Examples:

Purchases

Sales returns

Machinery

Rent

Bills Receivable

Credit Balances- Liabilities, creditors, capital, incomes and gains

Examples:

Sales

Purchases returns

Commission received

Bank overdraft

Bills payable

Methods of Preparing a Trial Balance

The three methods followed to prepare the trial balance are total method, balance method and

total-cum- balance method. We will learn only balance method in this section.

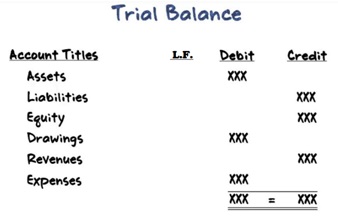

Balance Method for Preparing Trial Balance

A trial balance is prepared by depicting the balances of all the ledger accounts and placing the debit

and credit balances separately in the two columns. All the debit balances are recorded in the debit column

and all the credit balances are recorded in the credit column.

Specifics of Trial Balance

A trial balance is prepared on a particular date which should be mentioned on the top.

Name of the account should written in the first column.

The page number of the ledger where the balance appears should be written in the ledger folio column.

In the last two columns, the debit and credit balances are to be written.

Finally, the two columns are added up.

Points to Prepare a Trial Balance

Ledger and cash book are used to prepare the trial balance.

The balances of all accounts– assets, liabilities, capital, expenses and revenue accounts

(including cash balance and bank accounts) are placed in the debit and credit column of the

trial balance. An account with no balance is not recorded.

Opening stock account which has a debit balance is recorded in the debit column of the trial balance.

However, closing stock is not recorded in the trial balance and is given as additional information below

the trial balance. It shows the balance of unsold goods from the opening stock and purchases. In order to

incorporate the closing stock in the books of account, debit the closing stock account and credit thetrading

account by the amount of unsold stock at the end. In the balance sheet, closing stock appears as an asset on

the assets side of the balance sheet.

On the other hand, if the closing stock is to appear in the trial balance, then it needs to be adjusted through

purchases by debiting the closing stock and crediting the purchases account. Hence, closing stock is not shown

on the credit side of the trading account. However, it appears as an asset on the asset side of the balance sheet.

Accounts of assets with debit balance such as machinery, fixtures, land and building, bills receivable, good will,

trade mark, cash in hand, copyrights and patents are recorded in the debit column of the trial balance.

A debit bank balance is recorded in the debit column of a trial balance and a credit bank balance is recorded

in the credit column of a trial balance.

A credit balance of incomes and gains are recorded in the credit column and debit balance of expenses and

losses are recorded in the debit column of a trial balance.

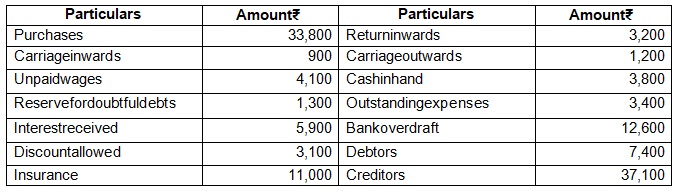

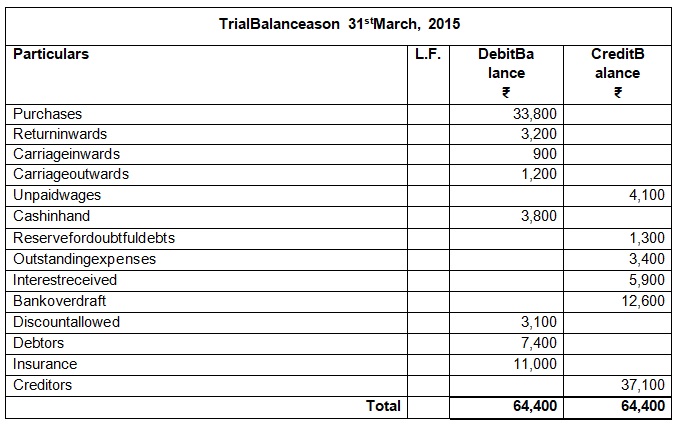

Prepare a trial balance of Mr. Ramesh from the given ledger balances as on 31St March, 2015.

Limitations of Trial Balance

A trial balance only shows that debit and credit balances are tallied. However, it does not mean that all the

recorded transactions and all the ledger entries, so made, are accurate.

It is not absolutely error free because certain errors may occur such as omission to enter a particular transaction,

incorrect journal entry or entry made to the wrong account.

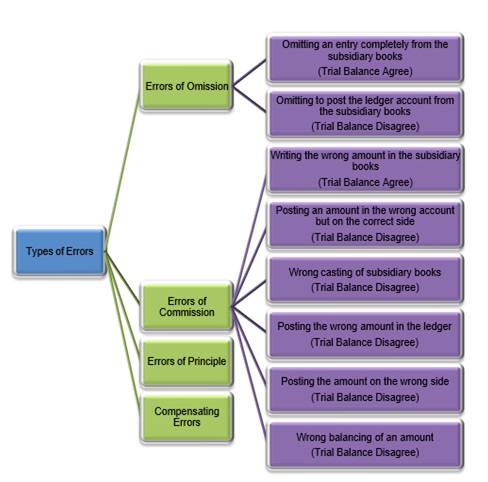

Classification of Errors

Errors of Omission

Error of omission is an error when a transaction is completely or partially missed from being recorded in

the books of account. Such errors are of two types:

Complete Omission: This error arises when a transaction is not recorded completely in the books of

accounts or if a transaction recorded in the journal is completely omitted to be posted in the ledger. This error

does not affect the trial balance. For example, cash worth ₹1,000 taken by the proprietor for personal use and

not recorded in the books.

Partial Omission: This error arises when a transaction is not completely recorded in the books or if the

entry is completely recorded but it may not be completely posted in the ledger of accounts. For example, ₹600

written off as depreciation on machinery and not been debited to depreciation account.

Errors of Commission

Errors of commission are committed because of wrong recording, wrong posting, wrong balancing and wrong casting

of subsidiary books. Such errors affect the accuracy of the trial balance.

Cash received from a creditor worth ₹5,000 is recorded in the cash book as ₹500. The transaction is recorded

in the cashbook as ₹500 instead of ₹5,000. This is an error because of wrong recording of amount in the cash book.

Amount received from Arun, ₹2,000, is wrongly posted in Tarun’s account. In this transaction, Tarun’s A/c is credited

instead of Arun’s A/c. This is referred to as an error of wrong posting of transactions.

Purchases returns book is totaled as ₹8,000 instead of ₹10,000. In this transaction, there is an error in totaling called

an error of casting.

The total of purchases returns book is carried forward as ₹6,000 instead of ₹2,000.This is an error committed in carrying

forward a total from one page to the next page. Such error called ’error in carrying forward’

Errors of Principle

Generally accepted accounting principles are to be followed while recording the accounting entries. When accounting

entries are recorded in contravention of accounting principles, it is known as an error of principle. For example, wages

paid for construction of building are debited to wages account

Compensating Errors

When two or more errors occur in such a way that the net effect of these errors on the debits and credits of respective

accounts are nil, it is known as compensating errors.

For example, on 2nd March, 2016, a sum of ₹2,000 paid to Ashok was posted as ₹200 to his account on the debit side

and on 26th March, 2016, a sum of ₹200 paid to Dipesh was posted as ₹2,000 to his account on the debit side.

In the first transaction, Ashok’s A/c was undercast by ₹1,800 on the debit side and in the second transaction Dipesh’s

A/c was overcast by ₹1,800 on the debit side. Hence, the net effect of these.

One Sided Errors

One-sided errors are those errors which affect the agreement of the trial balance. These errors affect only one account

and only one side i.e. debit or the credit side of the account. Errors of partial omission, recording transactions with

wrong casting and wrong posting are examples of one-sided errors. For example, goods worth of ₹3,000 purchased

for cash, correctly entered in the cash book, but while posting to purchase book, it is entered as ₹30,000. Thus, the

transaction has been recorded wrongly in the purchase book.

Two Sided Errors

Two-sided errors do not affect the agreement of the trial balance. These errors occur in two or more accounts.

Such errors are rectified by passing journal entries. Errors of complete omission, errors of principle and compensatory

errors are examples of two sided-errors. For example, credit purchases from Sohan of ₹15,000 were not recorded in the

purchases book; an error of complete omission because purchases account is not debited and Sohan’s account is not credited.

Steps to Identify the Errors

Recast the totals of debit and credit columns of the trial balance

Compare each account head and its amount appearing in the trial balance with that of the ledger to detect any

difference in amount or omission of any account

Compare the trial balance of the current year with that of the previous year to check the additions or deletions

of any accounts and to verify if there is any unexplained difference in amounts.

Re-check the correctness of balances of individual accounts in their respective ledgers.

Re-check the accuracy of the postings in individual accounts from the transactions entered in the books of original entry.

If the difference between the debit and credit columns is ₹1, ₹10, ₹100 or₹1000, the casting of the subsidiary

books should be re-checked.

If the difference between the debit and credit columns is divisible by 2, then there is a possibility that an amount

equal to half of the difference may have been posted to the wrong side of another ledger account.

The above point may also indicate a complete omission of a posting.

If the difference is divisible by 9, the mistake could be because of transposition of figures.

Still, if it is not possible to locate the errors, the difference in the trial balance for that moment is transferred to

the suspense account. All the one-sided errors detected are rectified through this account

Rectification of Errors

Errors may or may not affect the trial balance. However, they must be identified and corrected for the preparation

of final accounts. Rectification of errors is the procedure to rectify the errors committed and to correct the accounting

records. . The main objectives for rectifying the errors are as follows:

• To prepare correct accounting records

• To ascertain the profit or loss of the accounting period by preparing the profit and loss account with the correct amount

• To show the actual financial status of the company at a particular date by preparing the balance sheet with the correct amount

A. Errors may be classified under the following categories:

1. Rectification of errors before the preparation of the trial balance.

2. Rectification of errors after preparation of the trial balance but before the preparation of the final accounts.

♦ Rectification of Errors before the Preparation of the Trial Balance

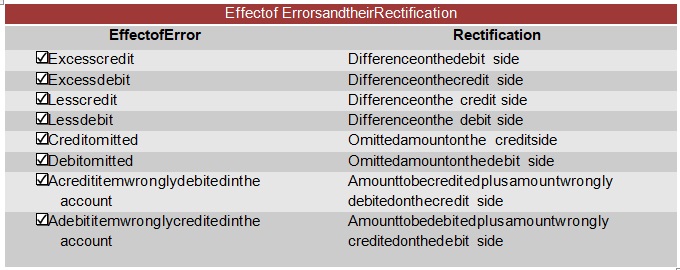

Errors which affect only one account or one-sided errors

One-sided errors are those errors which affect the agreement of the trial balance. These errors affect only one

account and one side i.e. debit or the credit side of the account. If these errors are identified before the preparation

of the trial balance, they are rectified by writing an explanatory note. Errors are rectified by debiting the relevant

account for short debit or excess credit and by crediting the account for short credit or excess debit. Examples of errors

which affect one account are casting, carry forward, posting, balancing and omitting to show an account in the trial balance.

♦ Rectification of errors caused by casting and carry forward

While carrying over the balance from one page to the next page, the error of carry forward or casting arises.

This error can be rectified by writing an explanation and by passing an appropriate entry.

For example, individual entries are correctly recorded in a sales return book but the totaling or casting of the

sales return book is undercast or overcast by ₹20,000. This error can be rectified by entering the amount in the

sales return account as To Undercasting of Sales Return Book ₹20,000.

KEY POINTS TO REMEMBER

► Errors are corrected before the preparation of the trial balance. Hence, the correction is made without

the help of suspense account.

► One-sided error can be rectified by passing a journal entry with the help of suspense account.

• Casting: The process of totaling the amount of all the transaction recorded at the end of an accounting period

is called casting. Purchases book, sales book, purchases return and sales return are posted in an individual

account such as purchases, sales, purchases return and sales return for a particular period i.e. the total amount

of all the books except cash and journal proper are posted to the ledger at the end of the accounting period.

• Errors of casting effect: Error of casting affects only the particular account to which the total of the book is

posted and where the total amount has been posted to the ledger. Here, the error may be undercasting or overcasting if

the total of the book is wrongly calculated.

• Undercasting:Undercasting of sales return book means under totaled amount in the sales return book.

This implies that the sales return account has been debited less with the amount of under total of the sales return book.

• Overcasting: Overcasting of purchases return book means over totaled amount in the purchases return book.

This implies that the purchases return account has been credited more with the amount of over total of the purchases return book.

• Occurrence of error in journal proper: Both the side entries of journal proper are posted with an individual

amount. For example, there is an error of omission in posting the transactions of journal proper, say machinery

purchased on credit from Mr. Ramesh for ₹1,20,000 was not posted. This implies that machinery account and Mr.

Ramesh account has not been posted.

♦ Rectification of errors of posting

Error of posting occurs while posting the entries from the subsidiary book into ledger account, an entry is completely

omitted to post or partially omitted to post or is posted with an incorrect amount or posted to an incorrect account.

These errors are identified with the help of certain key terms such as posted, debited and credited.

• Posted: The appropriate side of the account where the amount is to be posted.

• Debited: It stands for debit side of the account.

• Credited: It stands for credit side of the account.

♦ Rectification of errors of balancing

Error of balancing arises during the process of totaling the balance of an account. This affects the trial balance if an

incorrect balance of the account is entered in it. In order to rectify the error of balancing, an explanatory note is written

either on the debit side or credit side of the account as per the requirement

B. Two-sided errors which affect only two or more accounts

Two-sided errors are those errors which do not affect the agreement of the trial balance but arise in two or more

accounts. Such errors are rectified by passing the journal entries. Errors of complete omission, errors of principle,

errors of recording, errors of posting to wrong account and compensatory errors are examples of two sided-errors.

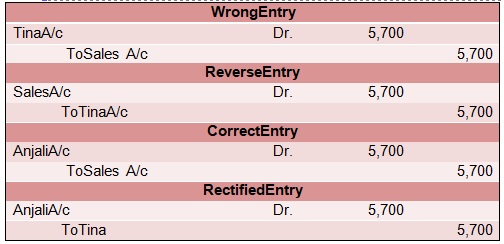

♦ Error of Recording

Error of recording arises at the recording stage in the subsidiary book. It affects the two accounts

i.e. in the first stage, incorrect recording affects the totaling of the book and this wrong totaling gets posted

and in the second stage, individual account is also incorrectly posted. For example, credit sale of ₹5,700 to Anjali

was recorded as sales to Tina.

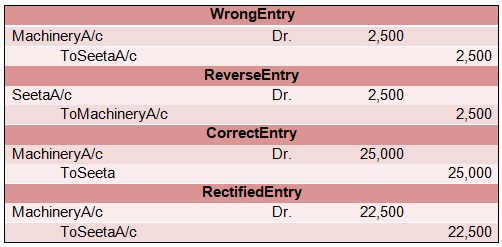

♦ Error of Posting to Wrong Account

Error of posting arises when a transaction is posted to the wrong account but on the

Correct side and with the correct amount

Correct side and with an incorrect amount

Incorrect side and with an incorrect amount

Incorrect side and with the correct amount

Here, an explanatory note is provided to rectify these errors. For example, machinery purchased on

credit from Seeta for ₹25,000 but posted as ₹2,500.

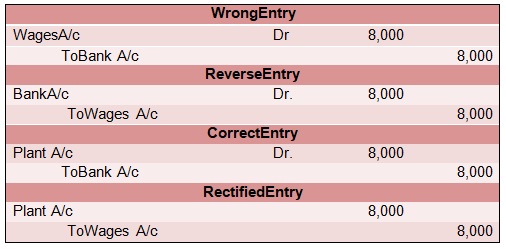

♦ Error of Principle

Error of principle arises during the allocation of expenditure or receipt between capital and revenue.

It does not affect the trial balance. Following points to be kept in mind during the allocation:

Purchase of an asset: Asset account will be debited but not purchases account

Purchase of an asset and expense incurred in purchase of that asset: Asset account will be debited but

not the expense account. If the expense account is debited, it can be rectified by crediting the expense account

and debiting the asset account.

Purchase of second-hand asset and if it has undergone repairing work before use: Here, the repairing charges

amount will be debited in the asset account but not in the repair account. If the expense account is debited, it can

be rectified by crediting the expense account and debiting the asset account.

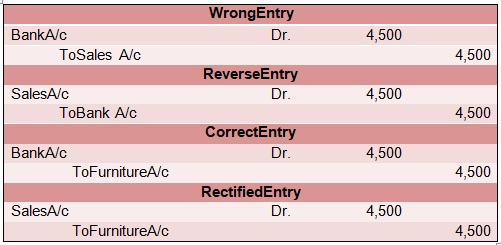

Sale of an asset: Asset account will be credited but not the sales account. If the sales account is credited, it will be

rectified by debiting the sales account and crediting the asset account.

Sale of an asset and its expense: Asset account will be debited but not the expense account.

For example, paid ₹8,000 for installation of plant debited to wages account

For example, sold old furniture for ₹4,500 was passed through Sales Book.

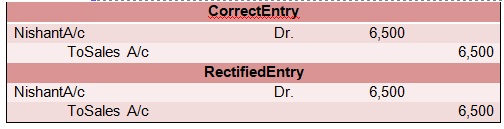

♦ Error of Complete Omission

Error of complete omission is directly recording the omitted transaction. For example, credit sale

of₹6,500 to Nishant omitted to be recorded in books

♦ Rectification of Errors after Preparation of the Trial Balance but before Preparation

of the Final Accounts.

• Errors not affecting the trial balance or two-sided errors are rectified by passing journal entry

without creating the suspense account.

• Errors affecting only one account or one-sided errors are rectified by

► Firstly, by placing the difference in the trial balance under the suspense account.

► Secondly, by passing the journal entry debiting or crediting the suspense account

Suspense Account

In certain cases, when the debit column and the credit column of a trial balance do not tally, the difference of

the trial balance is then transferred to a temporary account which is called a suspense account. This

KEY POINTS TO REMEMBER

► If error is committed in the subsidiary books, assume that the posting has been done as per therequirement.

► If error is committed in posting, assume that recording in the subsidiary book is appropriate.

account is created to avoid any delay in creation of the financial statements. If the debit column is less than the

credit column, then the suspense account is debited and if the credit column is less than the debit column, then

the suspense account is credited.

When all the errors are detected and rectified, the suspense account automatically gets balanced. However, when

errors still exist and are not rectified, the suspense account will not balance off and the balance amount of the suspense

account will have to be transferred to the balance sheet. The debit balance of the suspense account is shown on the assets

side and the credit balance is shown on the liabilities side of the balance sheet.

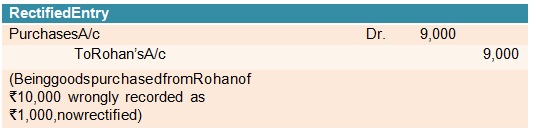

For example, purchases done from Rohan worth ₹10,000 recorded as ₹1,000. Here, the transaction is recorded for

₹1,000 instead of ₹10,000. This is an error of wrong recording of amount. Purchases A/c requires a further debit of

₹9,000 and Rohan’s A/c requires a further credit of ₹9,000. The rectifying entry is:

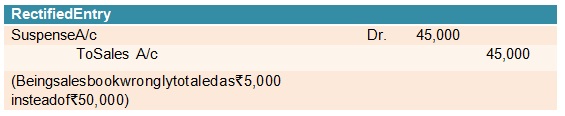

For example, sales book totaled as ₹5,000 instead of ₹50,000. Here, the total sales of the book are short by

₹45,000. This error can be rectified by any of the following two:

If the error is located before preparing trial balance, then ₹45,000 should be recorded in the credit side of sales account.

If an error is located after preparing the trial balance, then assuming that a suspense account is opened, the following

entry needs to be recorded.