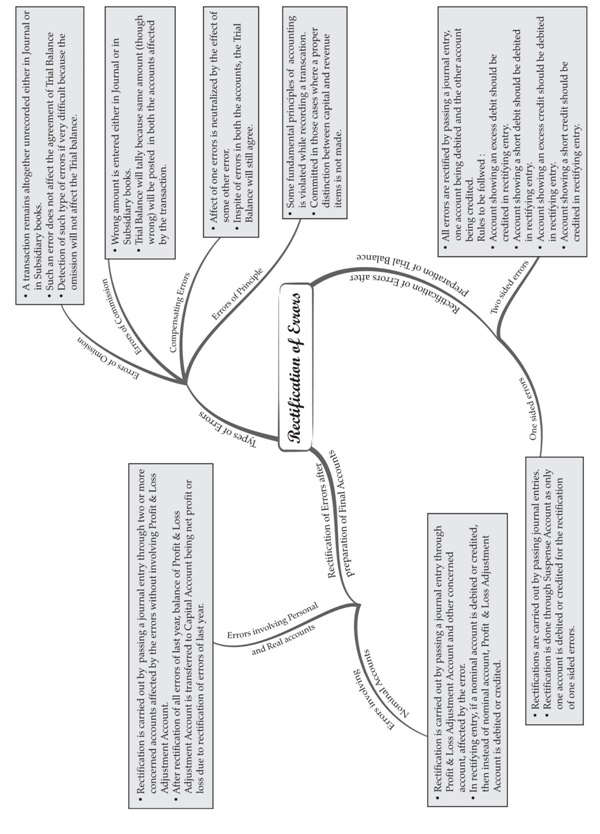

Financial Statements - II

Meaning of Adjustment entries:

Those entries which need to be passed at the end of the accounting year to show the accurate

profit or loss and fair financial position of the business.

Need for Adjustments:

Adjustments are required because sometimes payments and receipts made in the current year

may relate to previous or future years. So, these items must be adjusted so that the objectives of

financial statements can be achieved i.e., they depict true and fair financial performance of the business.

♦ Adjustments are required in the following items:

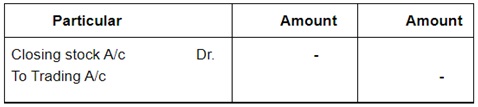

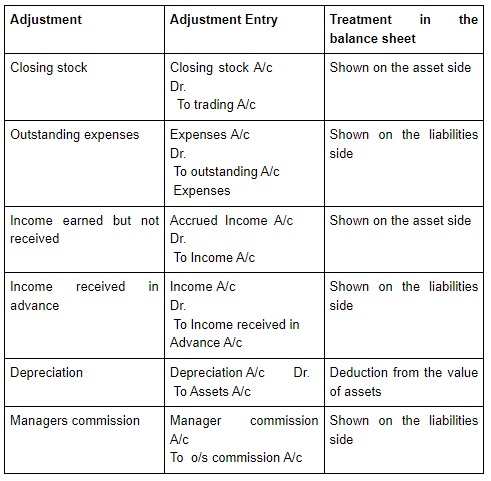

Closing Stock:

The closing stock represents the cost of unsold goods lying in the stores at the end of the accounting

period. The adjustment for the closing stock is done by

a. By posting it to the credit side of the Trading and Profit and Loss account

b. By posting it to the asset side of the Balance Sheet.

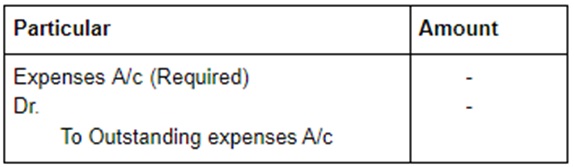

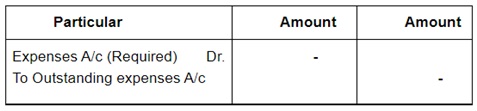

♦ Outstanding Expenses:

These are those unpaid expenses that the businesses haven’t paid in the present accounting period

and are due. The adjustment entry passed is:

Concerned Expense A/c……… Dr.

To Outstanding Expenses A/c

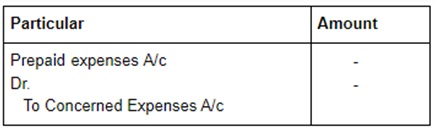

♦ Prepaid Expenses:

Expenses that are paid in advance i.e., those expenses which are paid in the current year but relate to

the next accounting year. For example, Rent Paid in Advance, Prepaid Taxes, Prepaid Insurance Premium,

etc.

The adjustment entry that is passed is:

Prepaid Expenses A/c………. Dr.

To Concerned expense A/c

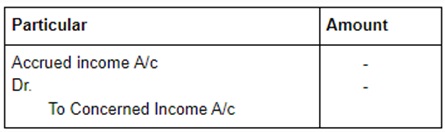

♦ Accrued Income: It may sometime happen that certain items of income such as a interest on loan,

commission, rent, etc. are earned during the current accounting year but have not been actually received

by the end of the same year. Such incomes are known as accrued income.

The adjustment entry that is passed is:

Prepaid Expenses A/c………. Dr.

To Concerned expense A/c

♦ Income Received in Advance: This is that income which is received in advance but not yet accrued.

The adjustment entry passed is:

Concerned income A/c …… Dr.

To Income received in advance A/c

The income received in advance is deducted from the respective income head in the Trading and Profit and

Loss Account and is shown in the liabilities side of the balance sheet.

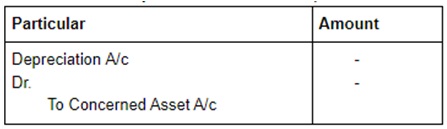

♦ Depreciation: Depreciation is the decline in the book value of the fixed asset because of regular wear and

tear and passage of time. The adjustment entry that is passed is:

Depreciation A/c ………. Dr.

To Concerned asset A/c

It is debited to the Profit and Loss Account and in the balance sheet the asset is shown at cost minus depreciation.

♦ Bad Debts: The debtors from whom amounts cannot be recovered are treated in the books of accounts as

bad and are termed as bad debts.

This is regarded as loss and the adjustment entry passed is:

Bad debts A/c ………. Dr.

To Debtors A/c

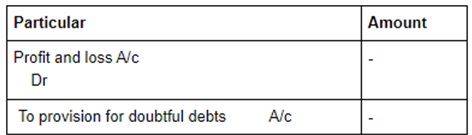

♦ Provision for Doubtful Debts: Sometimes we make a provision for some amount of Debtors that may not

realise in future such provisions are called provisions for doubtful debts. That Adjustment entry that is passed is:

Profit and Loss A/c ………Dr.

To Provision for doubtful debts A/c

♦ Provision for discount on Debtors: Discount is allowed to customers to encourage them to make prompt

payment. The discount likely to be allowed to customers in an accounting year can be estimated and provided

for by creating a provision for Discount on debtors.

The adjustment entry that is passed is:

Profit and loss A/c………. Dr.

To Provision for discount on debtors A/c

♦ Manager’s Commission: The manager of the business is sometimes given the commission on the net profit

of the company. The percentage of the commission is applied to the profit either before charging such commission

or after charging such commission.

The adjustment entry that is passed is:

Profit and loss A/c ………Dr.

To Manager’s commission A/c

♦ Interest on Capital: It is the interest that is paid on the capital of the proprietor. This interest is payable on

the capital that was at the beginning of the accounting year. And in case of any additional capital brought in by

the proprietor the interest is charged from the date it is brought. The adjustment entry that is passed is:

Profit and loss A/c………. Dr.

To Manager’s commission A/c

♦ Adjustment in Respect of Goods:

Abnormal Loss: Sometimes losses occur due to some abnormal circumstances such as accident, fire, flood,

earthquakes etc. Such losses are called Abnormal losses. These may be divided into two categories: -

(A) Loss of Goods (B) Loss of fixed assets

Good taken for personal use {Drawings in goods): When the goods are withdrawn by proprietor for

personal use the cost of such goods deduct from purchases and the amount should be deduct from capital in

Balance Sheet.

Goods distributed as free samples: Sometime goods are distributed as free sample by the businessman

for the purpose of advertisement. The cost of free sample deducts from purchase and shown in Debit side of

profit and loss account.

Important Questions

Multiple Choice Questions-

Q.1 Outstanding Expenses are related to-

(a) Current year

(b) Next year

(c) Last year

(d) None of these.

Q.2 Prepaid expenses are shown in-

(a) Liability side

(b) Asset side

(c) Assets or Liability side

(d) None of these.

Q.3 Charity of goods is-

(a) Expenses

(b) Loss

(c) Profit

(d) None of these.

Q.4 If a person fails to pay his debt, such amount is considered as-

(a) Bad debts

(b) Bad debts recovered

(c) Provision for Bad debt

(d) None of these.

Q.5 The object of non – trading concerns-

(a) Social service

(b) Profit earning

(c) Both of these

(d) None of the above.

Q.6 Such persons who earn remuneration against their services are called –

(a) Seller

(b) Purchaser

(c) Professional

(d) None of these.

Q.7 Which of the following is not an item of income of Non – trading concern –

(a) Entrance fees

(b) Interest

(c) Govt. Aid

(d) Salary.

Q.8 Receipt and payment account is a summary of-

(a) Income & Expenditure account

(b) Profit & Loss A/c

(c) Cash – book

(d) None of these.

Q.9 Which of the following is recorded in income & expenditure account –

(a) Revenue items

(b) Capital items

(c) Revenue and capital items

(d) None of these.

Q.10 The debentures to be redeemed within 12 months from the date of balance

sheet is shown under

(a) Short term borrowings

(b) Long term borrowings

(c) Other current liabilities

(d) Long term liabilities

Very Short-

1. Give any three points of superiority of Accrual Basis of Accounting over Cash Basis of Accounting.

2. Give a transaction that can break the Accounting Equation

3. Provide for all the possible losses but don't anticipate profits.' Identify the Accounting concept referred

in this sentence.

4. What is window dressing?

5. How does Cash book serve the dual purpose?

6. What is contra entry?

7. What do you mean by imprest?

8. Is Trial Balance the conclusive evidence of accuracy of accounting records?

9. What option is available to the accountant if Trial Balance doesn't match, and Final Accounts are to be prepared?

10. What is the nature of Suspense Account?

Short Questions-

1. Why do we need adjustments in financial statements?

2. What are outstanding expenses?

3. Pass the following journal entries.

a. Closing stock

b. Outstanding expenses

4. What do you mean by accrued income?

5. Give details of few items which need adjustments.

Long Questions-

1. Explain the following items with adjustments entry:

a. Closing Stock

b. Outstanding expenses

c. Income earned but not received

d. Income received in advance

e. Depreciation

f. Manager’s commission

Adjustment Entry Treatment in

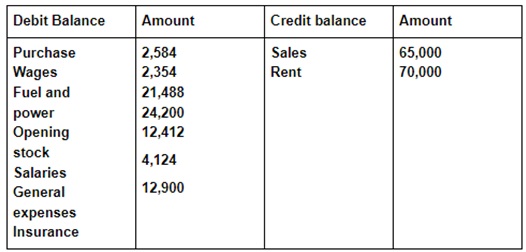

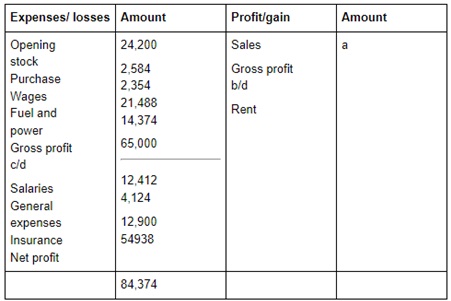

2. From the following balances prepare a Profit and loss account.

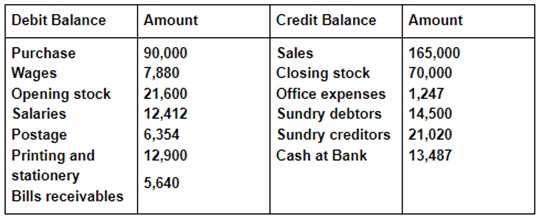

3. From the following balances, prepare the Profit and loss account and balance sheet.

4. Define following terms with adjustment entries:

Answer key

MCQ Answers-

1. Answer: (a) Current year

2. Answer: (b) Asset side

3. Answer: (b) Loss

4. Answer: (a) Bad debt

5. Answer: (a) Social service

6. Answer: (c) Professional

7. Answer: (d) Salary.

8. Answer: (c) Cash – book

9. Answer: (a) Revenue items

10. Answer: (c) other current liabilities

Very Short Answers-

1. Accrual basis of accounting considers all transactions cash transactions as well as credit transactions

whereas in case of cash basis of accounting only cash transactions are considered.

2. No transaction can break the accounting equation.

3. Prudence concept or conservatism concept.

4. Manipulation of accounting records to show a different picture is called window dressing.

5. All the transactions relating to cash and Bank are recorded in cash book in chronological order, so it becomes

a journal. All the transactions relating to cash and Bank can be checked at a single place with its balance, so it

becomes ledger also.

6. Contra entry is the entry recorded on both sides of cash book one in cash column the other in Bank column.

7. Imprest is the monthly advance given to the petty cashier for petty expense.

8. No, Trial Balance is not conclusive evidence of accuracy of accounting records. There can still be some errors

left after matching of the Trial Balance.

9. The difference in trial balance can be put to suspense account.

10. The nature of suspense account is not fixed as it is an artificial and Temporary account.

Short Answers-

1. Adjusting entries are used to bring accounts into compliance with the accrual principle. Some revenue and

costs may not have been recorded or updated at the end of the accounting period, necessitating the adjustment

of account balances.

Some revenue, cost, asset, and liability accounts may not represent their real values as presented in the financial

statements if correcting entries are not created. As a result, altering entries is required.

2. Outstanding expenses are those that have not been paid at the conclusion of the fiscal year. They're essentially in

relation to income earned during the current financial year. This expenditure becomes due to the firm when the benefit

has been received but the associated payment has not been made at the same time.

3. a. Closing stock

b. Outstanding expenses

4. Money that has been earned but not yet received is referred to as accrued income. By definition, mutual funds or

other pooled assets that accrue revenue over time but only payout to owners once a year are accumulating income.

Earned income is divided into two categories:

(1) items of income earned during the year, and

(2) items of However, it is not received at the end of the accounting year.

the same year's end.

5.The following are the things in the books of accounts that need to be adjusted:

• Defaulted debts

• Depreciation is the second type of depreciation.

• Earnings that have been accumulated

• Capital interest

• Earnings of the manager

• Closing the stock market

Long Answers-

1. Answer:

2. Answer:

3. Answer:

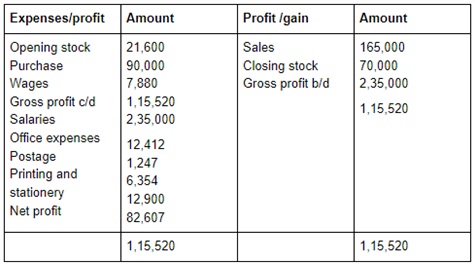

Trading Profit and loss A/c

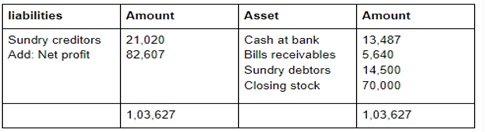

Balance sheet as of March 31

4. Answer:

A. Provisions for bad and doubtful debts.

Provision for bad and doubtful debts occurs when there is a possible reason for debtors who are doubtful

that they will not pay the debts on time.

B. Depreciation:

Depreciation means the value of an asset is declined due to its usage in the passage of time +9*or wear and tear.

It is usually treated as business expenses and is debited in profit and loss account.

C. Accrued income: The items of income that are earned during the accounting year but actually it is not received at the end of the same year.

D. Prepaid expenses: Prepaid expenses are the expense need to be paid in future, but they are paid in advance.

E. Outstanding expenses: Prepaid expenses are the expense need to be paid in future, but they are paid in advance.